Yes, joining the Freedom Debt Relief program can hurt your credit score. The reason is that Freedom Debt Relief negotiates debt when the credit is behind, thus affecting your credit score. We will cover all of that and more in this article. If you are wondering whether Freedom Debt Relief is a scam or whether Freedom Debt Relief lies, I would recommend reading our articles covering both of those topics.

Many people have started turning to debt settlement when they get fearful they won’t be able to fully pay back their debt without considering the potential consequences the settlement will have. One of the most significant consequences of debt settlement is credit score. Settling your debt can ruin your credit score, dropping it hundreds of points almost instantly.

This may not sound right. You did all the right things once you realized you couldn’t pay back your debt, right? You hired a reputable company to work on your behalf, you offered a payment, and you followed through with that offer! So why is your credit score still significantly lower? This article will tell you exactly why, and it will also help you find potential alternatives that could help protect your credit score from a sudden fall.

Freedom Debt Relief is one of dozens (if not hundreds) of debt settlement companies around the nation. Freedom Debt Relief claims to be able to help you settle your debt on your behalf. The way this works is relatively straightforward. Freedom Debt Relief tells you to stop making payments into your creditor. Instead, they open an Escrow account that you start making payments into. This is a very important step in the process for two reasons. First, becoming delinquent on your payments is typically the only way that your creditor will even entertain a negotiation. Second, if you have not missed any payments up until this point, this is the first thing that will begin negatively affecting your credit.

After you have made a decent amount of payments into the Escrow account, and you have missed an adequate amount of payments, Freedom Debt Relief will begin reaching out to your creditor and offering to negotiate. The process is successful when your creditor agrees to a negotiated repayment and the funds from your Escrow account are diverted to both your creditors and to Freedom Debt Relief (for their services).

Freedom Debt Relief does have decent ratings on Trustpilot, however it appears their Google Review function has been turned off.

Did you get a quote from Freedom Debt Relief, but don't know how much you are paying in fees? Did the individual just say that your fee is included in the monthly payment plan?

You may find that debt relief is right for you, but what if Freedom Debt Relief is charging you 25% of your enrolled debt compared to another provide that charges 15-20%? This could potentially results in thousands in additional fees.

As such, we built the following free debt settlement comparison calculator, so you can compare your Freedom monthly cost estimate to other debt relief providers? It also will give a clear estimate of your fees breakdown. The calculator also allows you to estimate the cost for credit counseling and bankruptcy.

Unfortunately, debt settlement does negatively impact your credit score. There is no way to get around it. If you decide to move forward with debt settlement, you are going to have to face the reality that your credit score will in fact be hurt. But what exactly causes a drop in your score? Here are the two biggest factors that impact your score:

One of the first things you have to do in order to move forward with debt settlement is to stop making payments on your debt. Even without going through with debt settlement, missing debt payments will decrease your credit score. What’s worse is that you can’t just miss one or two payments, it won’t be enough. You have to miss payments until your account is seriously delinquent which can take, at minimum, 3-4 months of missed payments. So, before you even begin the process of debt settlement, you can have around 4 months of missed payments hurting your credit score.

Consider where you are at with your current debt. Have you kept up with all payments so far? If this is the case, you may want to try any other form of debt relief before deciding to try and settle your debt. This can protect you from having missed debt payments listed on your credit report.

Once the debt is settled, the debt will no longer be listed on your credit report as delinquent or unpaid. It will, however, show that part of the debt was forgiven, which also hurts your credit score.

Again, this is another reason why other forms of debt relief may be better for your situation. If you think you can make some payments, but not the full payment each month, you may want to consider trying to find something that works for both you and the creditor. Adjusting your payment schedule won’t hurt your credit report nearly as much as a debt settlement would.

While there are definitely some scathing reviews that you can find on the internet claiming that Freedom Debt Relief is the only reason someone’s credit score was ruined, this doesn’t necessarily ring true. In fact, almost every single debt settlement company you work with will follow a similar pattern and end with a similar result. Unfortunately, the fact of the matter is that debt settlement can ruin your credit — regardless of who you are working with. This means that your score will be similarly affected, despite the company that you work with.

So, you may be wondering if there is anything else you can do. If debt settlement can ruin your credit score, is there something that won’t? Well, you do have options! While most debt relief processes will impact your credit score in some way, there are options that are minimally damaging. Here are just a few of those options:

Take some time to consider your financial situation. Consider writing out your income, expenses, and other monthly financial information. Do your expenses and debt outweigh your monthly income? If not, you may want to consider finding some help with debt management. Debt management can be as simple or as in depth as you want it to be. You can work with a financial counselor to figure out how to best organize your finances to ensure you are keeping up with your payments. This can help you feel more confident moving forward while paying off your debt.

While you don’t necessarily want to begin talking about settlement, there is a chance that you can talk to your creditor about the possibility of a revised repayment plan. Depending on whether or not the creditor decides to report the conversation or decision, there may be little to no impact on your credit. If you are able to pay part of your debt each month, offer that to your creditor. There is a chance that they will accept this smaller payment and allow you to pay off your debt over a longer period of time.

If you owe money on a tangible asset or thing, consider selling it! If you can get a decent price, you could potentially repay the loan without any consequence! Repaying the loan would not raise any red flags on your credit report and you would no longer be in danger of missing payments!

Now that we've covered alternatives and credit score impact, let's consider Freedom Debt Relief reviews.

Let's consider Freedom Debt Relief Reviews.

One thing to look into is how established the company is. Is their history solidified by time? Or are they relatively new? Some debt relief companies have stellar reviews. However, they have only been around for a couple of years, making their reviews not as reliable. A reliable debt relief company will have years of experience backed by generally positive reviews.

According to Freedom Debt Relief’s BBB page, the company was founded in 2003. Since then, the company has amassed thousands of reviews. The reviews span many different platforms, some of which we will look through below.

The Better Business Bureau is one of the most trusted review sites on the web. There are multiple factors considered by the BBB. There is also a place for client reviews and complaints, which helps make up the rating of each business. The BBB has given Freedom Debt Relief an A+rating, but the client rating is 4.3 out of 5 stars, which is averaged from the 1,428 client reviews.

It’s important to note that, while Freedom Debt Relief has been around for 19 years, BBB states that the accreditation date is 9/9/2021. Accreditation from the BBB isn’t difficult to receive — you simply pay a certain amount to become accredited. However, most legitimate businesses may opt to pay the amount in order to secure accreditation as it is something that marks the company as more reliable. Also, BBB accredited businesses receive grades based on client reviews and testimonies.

The number of reviews is very important to consider. When companies have a very small number of reviews, this could either speak to their newness, or to a general dissatisfaction with the company’s service. However, when the reviews of the company are still decent after thousands of client reviews, you can trust that the reviews are more reliable.

When looking at the positive reviews, clients claimed that Freedom Debt Relief was easy to work with, always available, and willing to talk through the process as many times as needed. Some negative reviews claimed that Freedom Debt Financial charged random fees without explanation and had difficulty canceling their contract.

Google reviews are less monitored than other platforms, meaning that anyone can publish a review without anyone verifying the information. Because of this, Google reviews tend to be much higher than other reviews.

Surprisingly, Freedom Debt Relief does not have any Google reviews to find. There are a couple of reasons this could happen. The first is that Freedom Debt Relief simply hasn’t created a Google My Business page. Setting this up allows for business information to be shown conveniently displayed when someone googles the name of the business. While this may be common for new businesses, an established business should have a Google My Business set up after 19 years.

Another possibility is that Freedom Debt Relief did have their Google My Business, but they were receiving an overwhelming amount of negative reviews. When this happens, Freedom Debt Relief can claim that they are being “attacked” with targeted negative ads. In order to protect businesses from unverified negative reviews, a company can take down their Google My Business.

Freedom Debt Relief’s Facebook page has opted to not have a reviews page. This means that people on Facebook cannot leave a review through the platform itself. Instead, they have integrated their Trust Pilot Reviews, which we will look at in the next section.

This could be seen as an issue. Social media is typically the easiest way for dissatisfied customers to leave a negative review. With both Google reviews and Facebook reviews turned off, there isn’t necessarily an easy way for a typical client to leave a review that is simple to access.

In an attempt to see how clients enjoyed working with Freedom Debt Relief — despite the reviews being turned off — I began reading through some comments on their most recent posts. Surprisingly, most of their more recent posts had many different individuals warning others to not enroll in the program.

One woman claimed that she started out with just over $30,000 of debt. However, she ended up with a grand total of $43,000 in debt AFTER she had already paid in about $17,000. Another claimed that, while he was trying to get into a debt consolidation program or even a debt settlement program, he found himself being pushed to apply for a loan instead. While he didn’t end up going through with any of the options, he claimed that the company was not paying attention to what he was asking for and were instead trying to pressure him into another high-interest loan.

Freedom Debt Relief has an astounding number of reviews on Trustpilot. However, it does appear as though they funnel all of their clients or potential clients to the site through both their website and their Facebook page. This could skew the ratings slightly.

Trust Pilot has given Freedom Debt Relief an average rating of 4.5 out of 5 stars. This is the average of almost 36,000 client reviews.

Trustpilot's positive reviews paint Freedom as a reliable, respectable company. About 91% of the reviews were either “Great” or “Excellent.”

Despite the majority of the reviews being good, the negative reviews were pretty incriminating. Many people complained that they were intentionally misled about what program they were entering into. Another user complained that the way Freedom Debt Relief set up their payment program forced them to take out a loan — a loan that was offered by a branch of Freedom Debt Relief. Other clients spoke of outrageous fees that doubled their debt. Some said they had lawsuits that could have easily been avoided. Others told of miscommunication between departments leading to the suffering of the client.

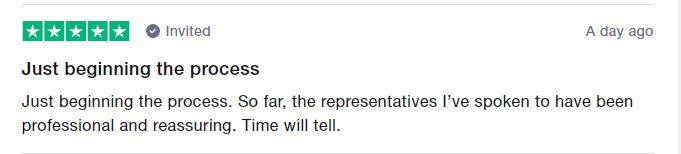

I think it is also important to note the content of the positive reviews. Despite thousands of positive reviews, it seemed as though the reviews mostly focused on initial contact and customer service. Many of the reviews stated that the individual had questions about the program itself. The individual claimed that whoever they were talking to was incredibly informative and helpful. In fact, on page one of the reviews, there is a woman who gave a stellar, 5-star review but admits she has only just begun the process (see image below).

While this isn’t inherently bad, it does speak to the importance of knowing when a review was written. As you can see in the screenshot above, Trustpilot shows that this reviewer was invited to review Freedom Debt Relief. Knowing that Freedom Debt Relief invites individuals to review their services as soon as the initial point of contact shows that their positive reviews may be overwhelming because their upfront customer service is so good and they ask for fast reviews — especially before they do any debt settlement.

Though this is an incredibly skeptical take on the reviews found on Trustpilot, I don’t think it is an unfair one, especially based on the content of the written reviews. Most speak as though not much has happened yet, but that the individual is excited for the future. Which… of course — they’ve just been told they could have thousands of dollars of debt vanish! Regardless of how you interpret the data, it is important to think critically through the possibilities.

Obviously, employees experience a different side of the company. However, it still is important to check and see if they have anything to say about them. Unfortunately, Freedom Debt Relief is a part of Freedom Financial, so we cannot simply view the reviews of the debt relief branch. However, there are still some reviews on the Glassdoor Freedom Financial page that are worth considering.

One employee claimed that the Upper Management at the company had no interest in their employees or the clients they were working for.

Overall, the employee rating for Freedom Financial is only a 3.9 out of 5. Hwever, this again encompasses all of Freedom Financial and not just Freedom Debt Relief.

Ultimately, Freedom Debt Relief does have decent online customer reviews. However, there are a few issues that may cause some hesitation. The first is that no Google reviews are available for an otherwise well-established company. Secondly, both Freedom’s website and Facebook page only pull reviews from one source (Trustpilot), which has a high number of positive reviews. Thirdly, of the almost 36,000 reviews on Trustpilot, almost every single positive review was from someone who was invited by Freedom Debt Relief to review on the site. From the front page alone, it was easy to see that a lot of the reviews were made either directly after the first point of contact OR sometime soon after.

All of these things are worrisome, despite the massive amount of positive reviews. In the end, however, the decision is up to you. Freedom Debt Relief is a well-established company with over 19 years in the business. If you are still wanting more information on Freedom, give them a call or continue researching for more honest opinions on Freedom Debt Relief’s services. Consider asking around and trying to find a trusted friend or acquaintance who has worked with Freedom before to hear about their experience! Whatever you decide to do, remember that a step towards debt relief is a good step. Hopefully, we can help you make that step with confidence.

If you have any questions or want to talk with someone about your debt-relief options, we would love to help. Give Ascend a call and you can talk — for free — with someone about your unique situation.