Many people think of having to file bankruptcy as a failure, I thought the same thing myself until I had to file for bankruptcy protection. The process was quite simple and easy, much easier than anything I read on the internet. My spouse and I filed chapter 7 bankruptcy in June of 2022, we received our discharge 91 days after our file date in October of 2022.

Throughout the duration of our bankruptcy everything that was included in our bankruptcy petition had the balances zeroed out, and all negative information was deleted. The only ‘negative’ item that was left were in the remarks of each account which stated, “Chapter 7 Bankruptcy.” Upon the discharge of our bankruptcy a few accounts started to report again as open even though they were included in the bankruptcy, and they should be closed. I had a creditor try to collect on a debt after my discharge.

I will walk through a few errors that I found on my credit report and what I am going to do to fix them as well as how I responded to the creditor who tried to collect from me.

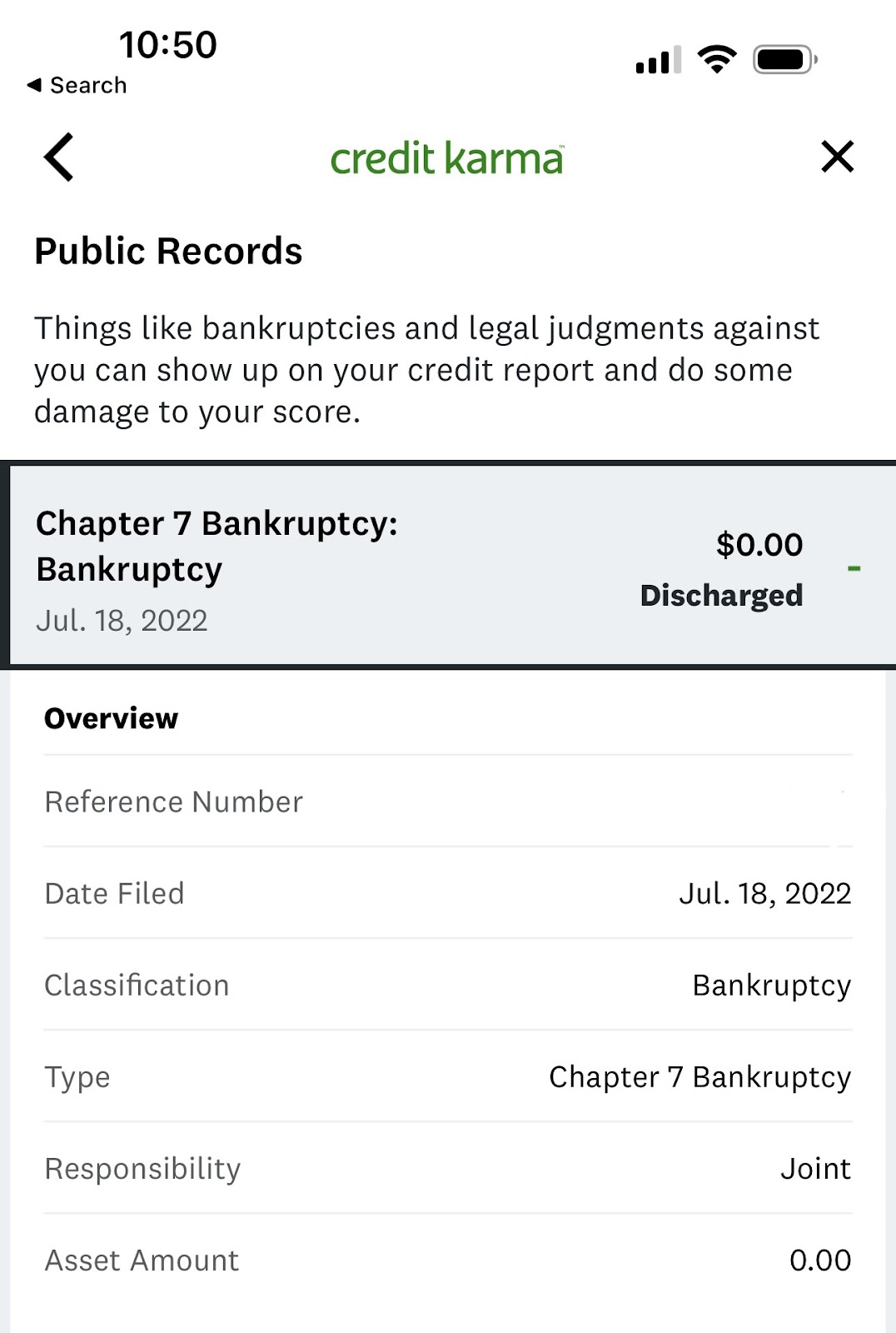

What Does Bankruptcy Look Like On Your Credit Report?

This is what bankruptcy looks like on your credit report, it may vary depending on which credit checking site you are using. This is what it looks like on Credit Karma:

How Accounts Included in Bankruptcy Should be Reported

Accounts that are discharged in your bankruptcy may have remarks such as:

- Chapter 7 or 13 Bankruptcy

- Discharged in Bankruptcy

- Discharged

They may also report the account as a negative item, but with a zero balance. The accounts will be deleted off your credit report in 7 years, but the bankruptcy could remain on your credit report for 10 years if you filed chapter 7 or 7 years if you filed chapter 13.

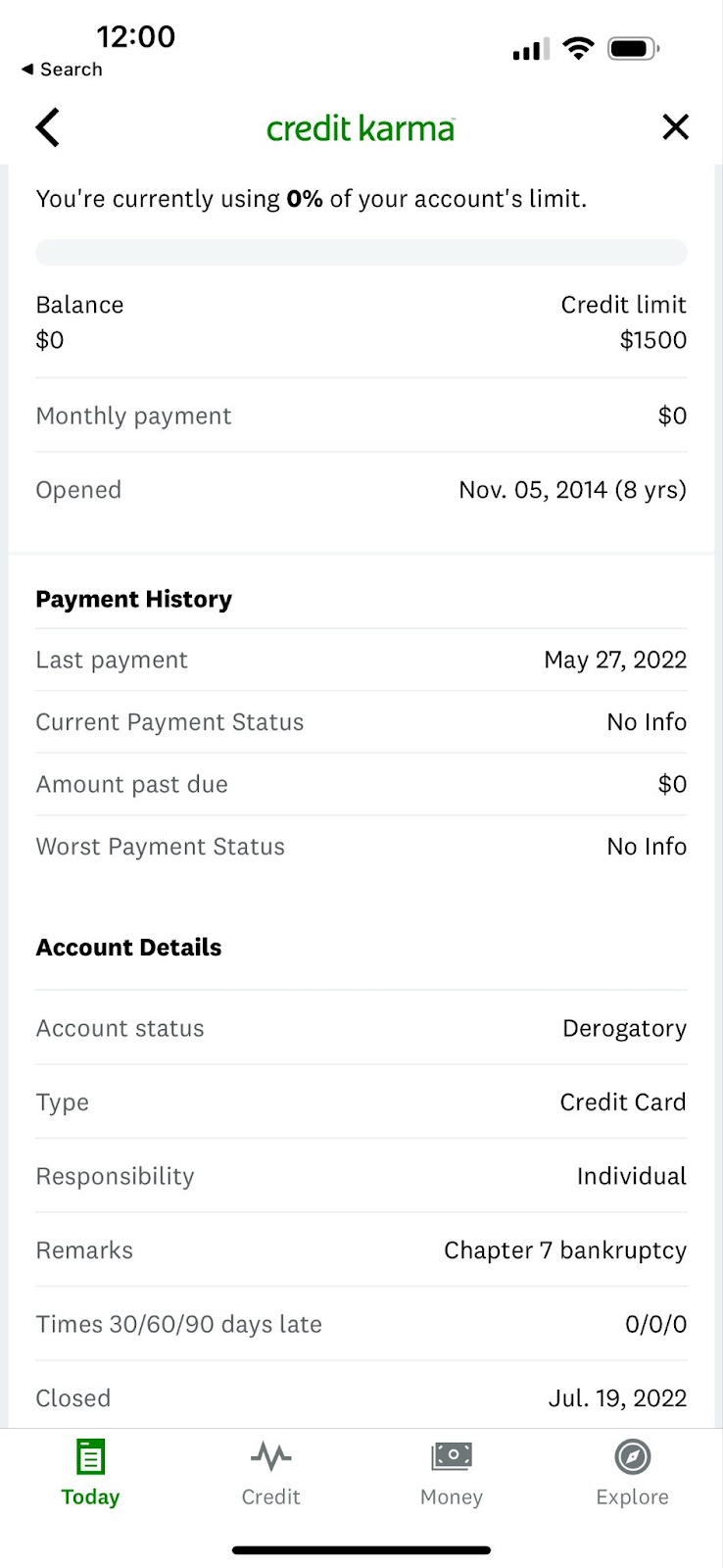

Here is an example of account remarks for an account that was included in bankruptcy and is reporting correctly:

Inaccurate Reporting of Accounts Included in Bankruptcy

When your bankruptcy gets discharged, there may be some errors which is normal. We discussed above how accounts should be reported, here are some remarks that are not accurate and should be disputed:

- Currently Owed

- Active

- Open

- Balance Owed

- Delinquent

- Outstanding

- Charged off

- Reporting with a balance owed. It is illegal for creditors/debt collectors for trying to collect on a debt that was discharged in bankruptcy, it is also illegal for them to report your account as open or with a balance.

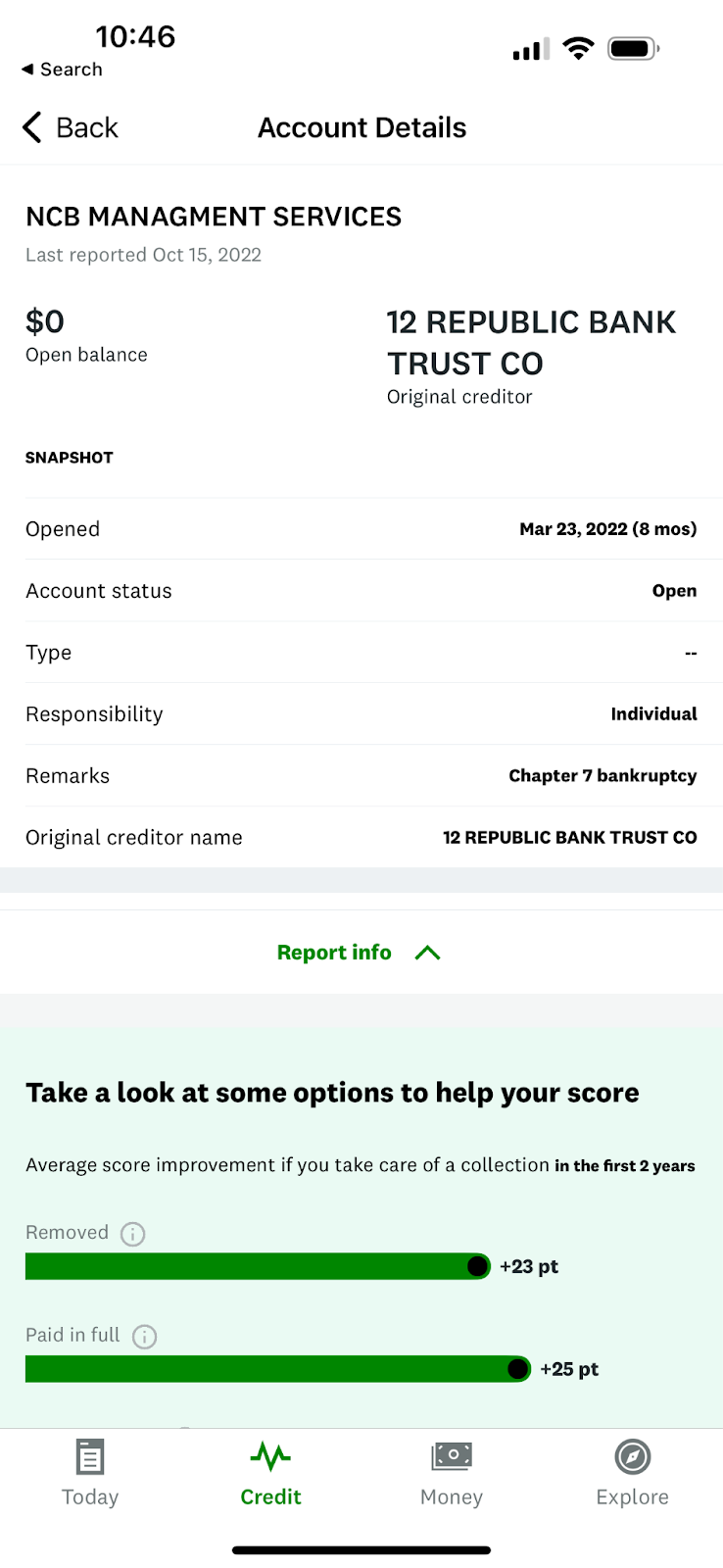

Prior to filing for bankruptcy, we had a few accounts that went into collections, while my bankruptcy was open, they were not reporting. However, now they are reporting as “open” but with a zero balance. They should be reporting as closed since they were discharged in the bankruptcy. Here is an example of the collection account that is reported as “open” but with no balance:

How to Fix Errors with Reporting After Bankruptcy

It is very important that you work to report any errors that you find on your credit report after bankruptcy. Your credit may rebound much quicker if all inaccurate information is dealt with. I chose to mail in my disputes to all 3 of the credit bureaus (TransUnion, Experian, and Equifax). I chose to mail in my disputes because I could send them via certified mail with a return receipt requested that way I knew they received my disputes. Below is a copy of the dispute that I sent all 3 credit bureaus. I got this sample from the Federal Trade Commission Consumer Advice website. Basically all you have to do is fill in the blanks and then mail it. You can copy the example bellow, just replace the items that are bolded with your information. For the enclosures or “evidence” I just attacked a copy of my original bankruptcy petition and highlighted the accounts in question and then also sent in copy of my discharge paperwork. Here is the example:

[Date]

[Your Name]

[Your Address]

[Your City, State, Zip Code]

[Credit Bureau Name]

[Street Address]

[City, State, Zip Code]

Subject: Disputing Information in Credit Report

I am writing to dispute the following information in my file.

This item [for instance: retailer account at ABC Department Store] is inaccurate [or incomplete] because [describe in detail what is inaccurate or incomplete and why]. I am requesting that this item be removed [or request another specific change to correct the information].

[List and describe any other items you are disputing.]

Enclosed is documentation supporting my request: [describe the documents you’re sending, for instance: my credit report, with the disputed items circled.]

Please investigate this matter and delete [or correct] the disputed item[s] as soon as possible.

Sincerely,

[Your name]

Enclosures: [List what you are enclosing]

These disputes were sent out about 3 days ago, I will write a follow up article describing my results and any further action I needed to take.

Can A Debt Collector Collect On A Discharged Debt?

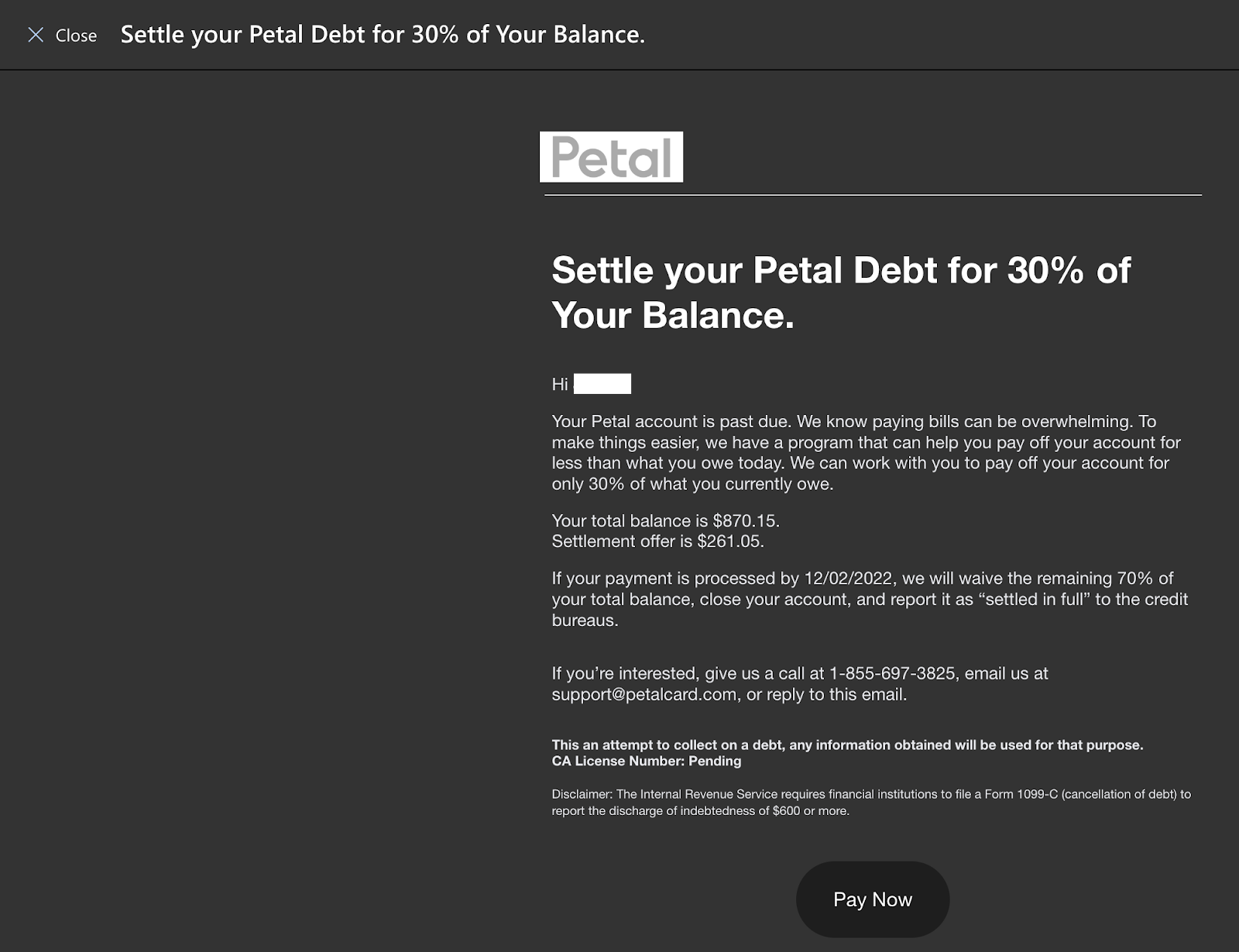

After my discharge one of my accounts that I had tried to collect some money from me. They sent me a settlement offer via email, I did some research and found out how to respond. I responded to their email with a very generic email stating that I filed bankruptcy, the account in question was discharged, my case number and my attorneys information. I waited 72 hours and they were still reaching out. I did some research and I found that The Consumer Financial Protection Bureau had a template on their website that I was able to adapt to my situation and send off to them. Here is an the email that the debt collector sent me:

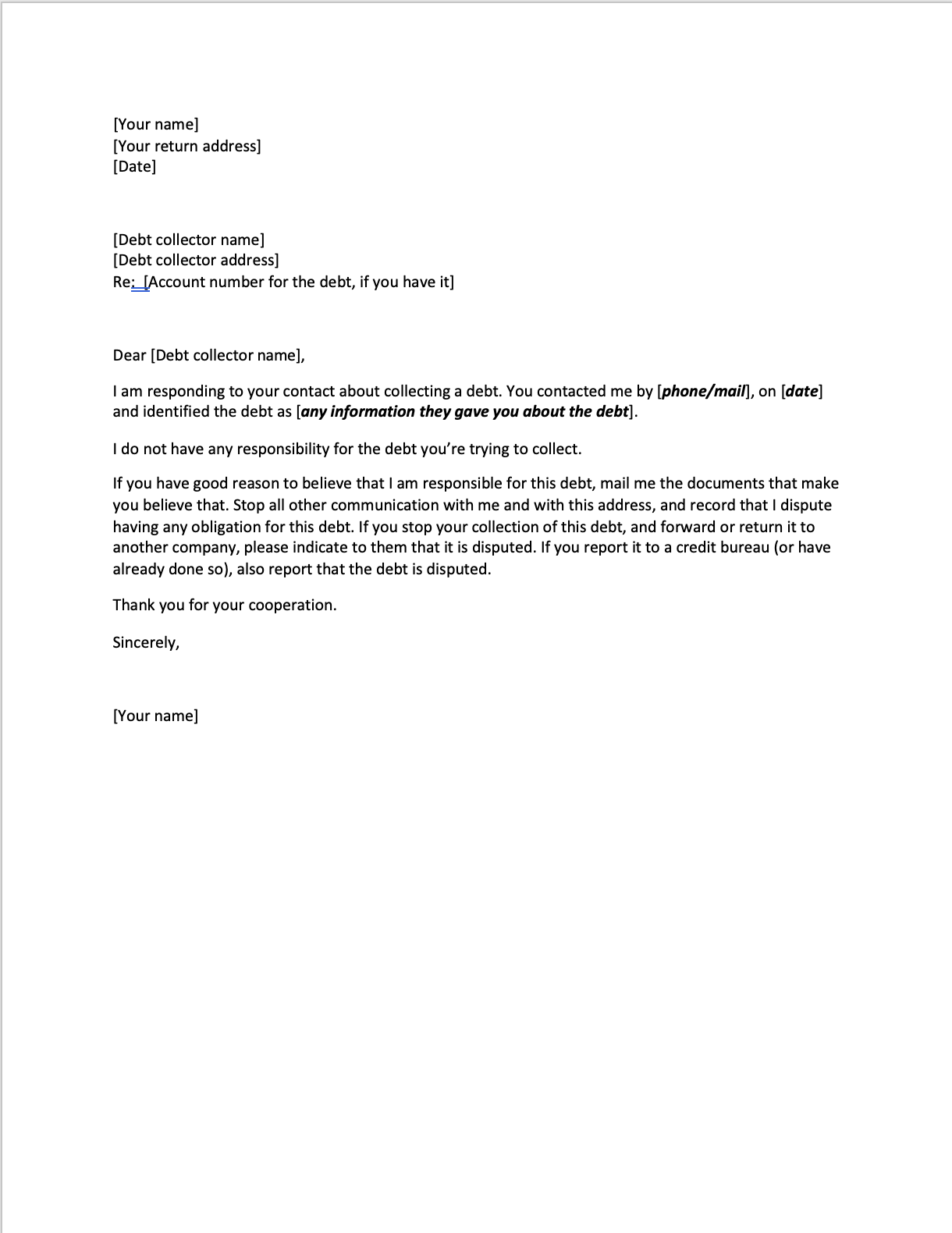

Next I will show you the template I used for my response. The only modification I made is that I added that I filed chapter 7 bankruptcy, the date I filed, the date it was discharged, my case number and my attorneys information. You can see the sample here:

This template was so straightforward and easy to use, I just replaced the bolded parts with information that pertained to me, and my situation. I sent this letter via certified mail and I requested a return receipt requested. That way I would be positive that they received the dispute and that they are in violation of the Fair Debt Collection Practices Act.

Conclusion

All in all I am very happy that I filed for bankruptcy. It was long overdue and I wish I would have done it sooner. The whole bankruptcy process was very easy and not time consuming, in the past I never paid much attention to my credit report and whether or not information was correct. It is very important that everything is reporting accurately on your credit report a 5-10 point difference can save you a lot of money. It can move you from sub-prime to prime, which can save you thousands of dollars across the life of your loan.

If you are in a similar situation or have not filed for bankruptcy yet and want some unbiased free advice, reach out to our team at Ascend! Give us a call at 833-272-3631 and we can schedule a call with you! You can also use our free Chapter 7 vs Chapter 13 Bankruptcy calculator below to see if you qualify and a price estimate if you have not yet filed.